Global Energy Realignment: From Russian Oil & Gas to US LNG and Oil

The global energy landscape has undergone a profound transformation in recent years, accelerated by geopolitical conflicts, supply disruptions, and strategic policy shifts. The Russia-Ukraine war triggered an initial pivot away from Russian pipeline supplies in Europe, while the 2026 escalation involving Iran and the Strait of Hormuz has reshaped oil flows, elevating the United States as the primary beneficiary and swing supplier. This realignment is evident in surging US LNG exports to Europe, growing US energy footprints in India, massive draws on strategic petroleum reserves (SPRs), and record declines in global oil inventories.

Europe’s Shift: Russian Gas Out, US LNG In

Europe’s energy security strategy crystallized after 2022. Russian pipeline gas imports plummeted from approximately 165 billion cubic meters (bcm) in 2019 to just 20 bcm by 2025, creating a massive 145 bcm supply void. US LNG exports filled a significant portion of this gap, exploding 16-fold from 5 bcm to 81 bcm over the same period. The remainder came from Norwegian pipeline gas, Qatar, and North African sources. By recent years, US LNG accounted for over half of EU LNG imports.

This transition has been locked in through long-term contracts and high-level diplomacy. A landmark EU-US trade deal aims for $750 billion in American energy purchases through 2028. Projections from the Institute for Energy Economics and Financial Analysis (IEEFA) suggest the US could supply around 80% (~115 bcm annually) of EU LNG needs by 2030. Qatar’s Ras Laffan terminal, reportedly damaged by Iranian attacks, faces 3–5 years of reduced capacity, further cementing reliance on American cargoes. US LNG exports have hit record levels near 20 billion cubic feet per day (bcf/d).

(Source of Image/Data: themerchantnews.com)

While this has enhanced energy security for Europe, it has come at a cost: higher prices for seaborne LNG compared to cheap Russian pipeline gas, contributing to industrial pressures and inflation. The shift also reinforces transatlantic energy interdependence but exposes Europe to global LNG market volatility and shipping risks.

India’s Diversification: Rising US Share in LPG and LNG

India, one of the world’s fastest-growing energy consumers, is mirroring aspects of this diversification. Traditionally reliant on Qatar for LNG, India has broadened its sources amid rising demand from power generation, fertilizer production, and city gas distribution networks. Data from Kpler highlights the growing US presence. In India’s LNG imports (million tonnes), the US share (dark blue) has expanded noticeably from early 2025 through May 2026, alongside contributions from UAE, Oman, Nigeria, Angola, and spot cargoes from Others. Qatar which was once dominant player in Indian LNG is no longer overwhelmingly dominant.

Even more striking is the surge in LPG imports from the US. From December 2025 to May 2026, US LPG volumes to India rose sharply: 182.7 (’000 tonnes) in Dec-25 (8.1% of total), climbing to 268.8 in Jan-26 (11.9%), 289.7 in Feb-26 (14.4%), 435.1 in Mar-26 (36.9%), 384.9 in Apr-26 (39.6%), and peaking at 665.8 in May-26 (54.7% of total imports). This growth reflects both policy-driven diversification away from discounted Russian crude and practical supply needs amid Middle East disruptions. India has faced challenges with higher refining and landing costs for US shale crude and Venezuelan barrels, but the volumes underscore a strategic pivot.

(India’s LNG Imports - Source: Kpler)

The 2026 oil crisis, triggered by Hormuz disruptions, forced non-Gulf suppliers including the US to ramp up sharply. Gulf producers suffered severe export losses: Iraq (-3,000 kbd), Saudi Arabia (-2,700 kbd), Kuwait (-1,300 kbd), and UAE (-400 kbd). The US surged by over +2,000 kbd, part of a broader Atlantic Basin response to a 12–14 mb/d global shortfall.

The 2026 Oil Crisis: Hormuz Disruptions and SPR Drawdowns

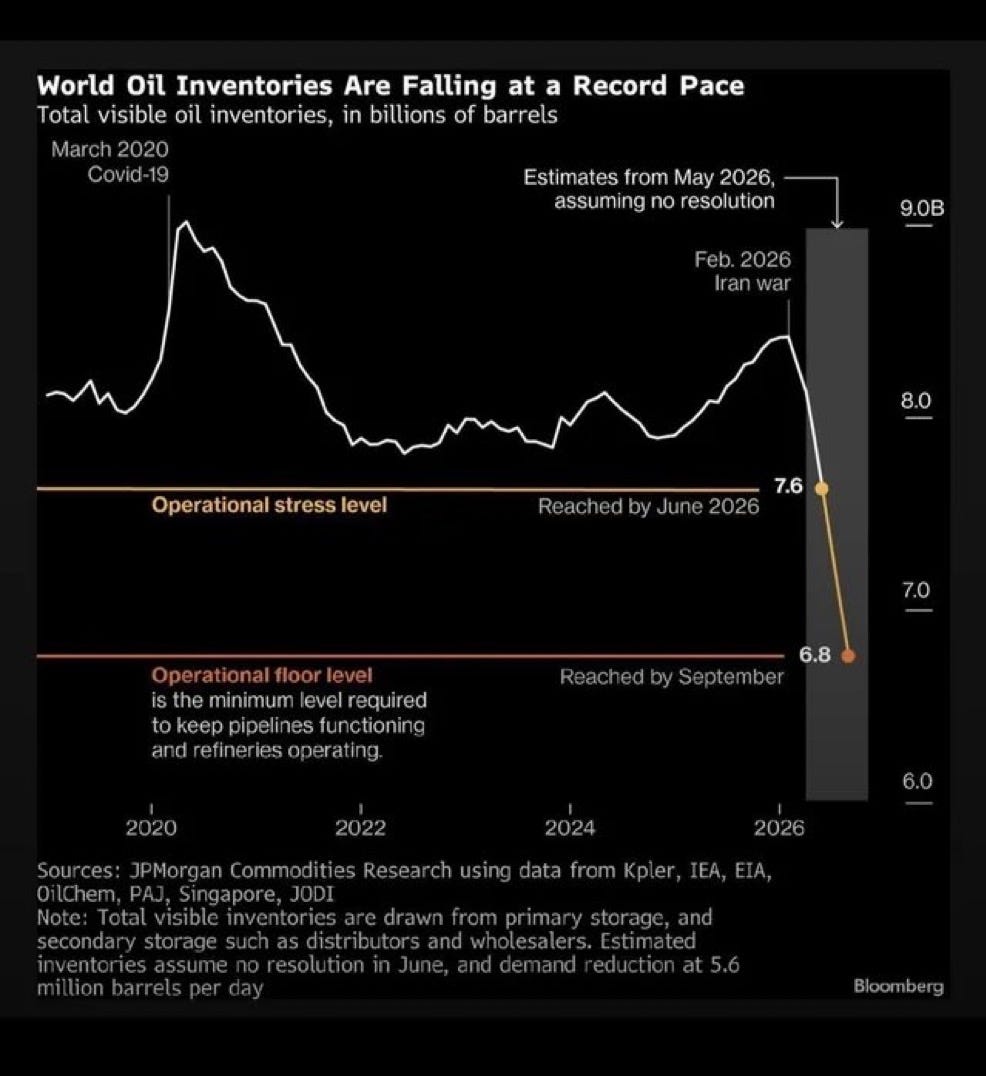

The conflict centred on Iran and the Strait of Hormuz has caused massive oil export disruptions. With key chokepoints affected, global supply tightness has intensified. World oil inventories are falling at a record pace. Total visible inventories, which stood higher in early 2026, reached the operational stress level of 7.6 billion barrels by June 2026 and are projected to hit the operational floor of 6.8 billion barrels by September, assuming no resolution. This floor represents the minimum required for pipelines and refineries to function.

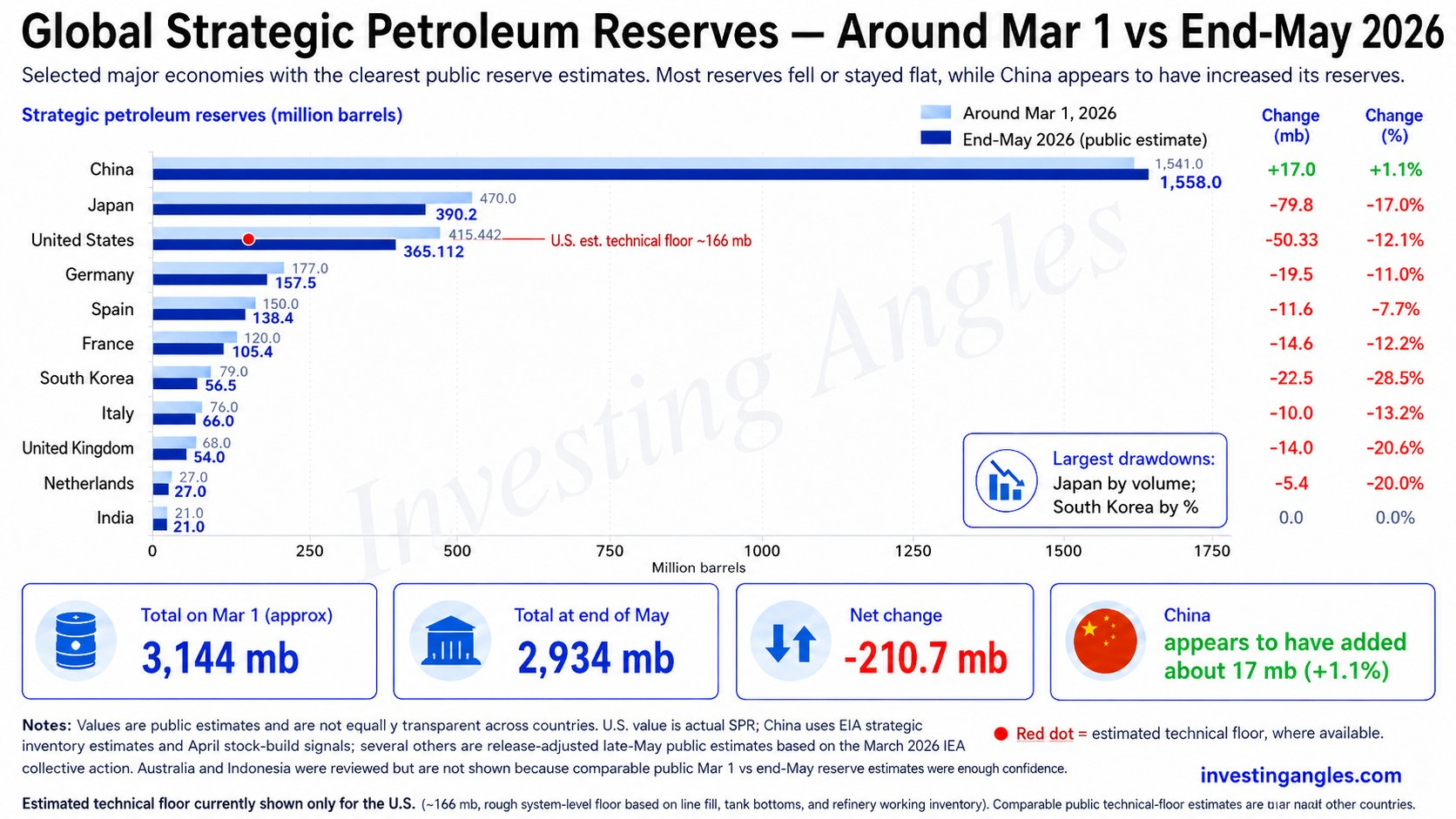

Strategic reserves have been heavily mobilized. Between early March and end-May 2026, global SPRs fell by a net 210.7 million barrels, from 3,144 mb to 2,934 mb. Major economies drew down: Japan (~80 mb, -17%), United States (~50 mb, -12.1%), Germany, France, and South Korea also released volumes under coordinated IEA efforts. China notably increased its reserves by ~17 mb (+1.1%), reaching 1,558 mb. India’s reserves remained stable at 21 mb.

(Source of Image/Data: investingangles.com)

The United States has been particularly aggressive in tapping its Strategic Petroleum Reserve (SPR). Inventories fell from around 415 million barrels earlier in 2026 to 384.1 million barrels, with weekly draws peaking at 9.9 million barrels. The SPR’s total capacity is 714 million barrels, with a maximum draw rate of 4.4 mb/d but a slow refill rate of ~0.8 mb/d. Analysts warn that continued draws risk plunging reserves to the 2023 modern low of 347 million barrels by late June or mid-July 2026, approaching the policy floor of 238 million barrels and threatening structural integrity of the salt caverns.

Global oil inventories appear substantial but are far more constrained than headline figures suggest. According to JPMorgan Commodities Research, drawing on data from Kpler, IEA, EIA, and other sources, total visible inventories stood at approximately 8.4 billion barrels at the start of 2026. However, only about 800 million barrels represent a truly flexible, usable buffer. The vast majority is locked as essential working inventory pipeline line pack, tank bottoms, refinery minimum operating levels, and logistical requirements. By late April 2026, roughly 280 million barrels of this usable cushion had already been consumed amid the Hormuz disruptions. The situation has worsened since, with inventories hitting the Operational Stress Level of 7.6 billion barrels by June 2026 and projected to reach the Operational Floor Level of 6.8 billion barrels the minimum required to keep pipelines pressurized and refineries functioning by September 2026 if the crisis persists.

Compounding the pressure is the rapid depletion of the US Strategic Petroleum Reserve (SPR). As of late May 2026, the SPR stands at approximately 365 million barrels, down from 415 million barrels earlier in the year. At the current draw rate of 8–10 million barrels per week (1.2–1.4 million barrels per day), the reserve is on track to hit the policy floor of around 243 million barrels by mid-to-late August 2026. Falling below 150–200 million barrels would risk structural damage to the salt caverns and severely limit emergency response capability. While the SPR has provided a vital temporary buffer to support exports and moderate price spikes, its accelerated drawdown highlights the fragility of global energy buffers. Breaching these operational floors and reserve thresholds risks widespread logistical breakdowns and heightened market volatility through the remainder of 2026.

Geopolitical and Strategic Implications

The US has capitalized on these disruptions to strengthen its position as the world’s swing supplier. In both gas and oil, American producers, exporters, and infrastructure developers have gained significantly. Europe has traded Russian pipeline dependence for costlier LNG reliance. Asian importers, including India, have faced price spikes and reserve drawdowns, while Gulf economies have endured major revenue losses. Washington appears to be leveraging the crisis on multiple fronts.

First, US is converting key buyers like India into more captive markets for US shale crude, Venezuelan barrels (despite higher costs), and LNG, while using trade deals and sanctions threats to discourage discounted Russian oil imports mirroring its EU playbook.

Second, challenging the traditional Gulf-dominated Middle East energy order to reinforce the petrodollar system and pressure nations like India and China to abandon non-dollar mechanisms such as the Petro Yuan or Rupee-Rouble trade loops for American Oil & LNG in dollar pipeline.

Third, America is aiming to restructure global energy supply chains which fuel the AI and data centre boom. Its treating energy as critical infrastructure for the Fourth Industrial Revolution and thus by controlling the energy supply chains to dollar denominated oil & gas supplies America is aiming to re-assert is global dominance.

However, this strategy carries risks too like US is draining its SPRs at a record pace leaves the US and allies vulnerable to future shocks in weeks and months ahead. Physical crude tightness, with Hormuz flows unlikely to resume soon, will likely push prices higher as screen values of Brent will align with actual barrel costs. Unless the Americans are able to strike a deal with Iran and Hormuz opens soon the world is staring at an energy crisis where countries could be forced to liquidate its US Treasury holdings just like what Turkey did few weeks back when its Lira went into a free fall. The moment of reckoning for American & the global economy is fast approaching.

Outlook and Challenges

The United States taking this Iran war crisis as an opportunity is actively attempting to restructure global energy supply chains, positioning itself as the indispensable swing supplier in an era defined by the Fourth Industrial Revolution (IR 4.0). With AI infrastructure and hyperscale data centres demanding vast, reliable baseload power, Washington views secure, dollar-denominated energy flows as critical infrastructure. Through surging LNG exports to Europe, growing LPG and crude sales to India, and sanctions pressure, the US aims to lock partners into long-term dependencies that support both energy security and technological dominance. Yet this vision faces substantial resistance in a multipolar world. Major powers like China, India, and Russia are determined to maintain strategic hedges and autonomy rather than place all their energy eggs in the American basket.

China has capitalized on the crisis by expanding its strategic petroleum reserves by approximately 17 million barrels between early March and end-May 2026, reaching an estimated 1.3–1.4 billion barrels. Beijing continues to secure Russian crude through alternative tanker routes and advances non-dollar payment mechanisms, preserving its ability to withstand prolonged disruptions without over-reliance on US or Atlantic Basin supplies. China’s SPR is 3X of United States and it is also getting regular oil supplies from Iran through land as well some tankers through Strait of Hormuz which US navy is allowing to pass through.

India embodies pragmatic multi-alignment. While US LPG imports have risen dramatically reaching 665.8 thousand tonnes and 54.7% of total imports in May 2026 and its share of LNG is growing, New Delhi continues importing Russian oil and diversifying LNG sources across Qatar, UAE, Oman, Nigeria, Angola, and spot markets. Higher refining and logistics costs for US shale crude and Venezuelan barrels have not displaced cheaper alternatives. India’s approach prioritizes energy autonomy and cost efficiency over exclusive alignment with Washington.

Russia, despite sanctions, sustains alternative trade loops such as the Rupee-Rouble mechanism and reroutes exports to Asian markets, remaining a relevant player in the global energy balance. Russia continues to be the main supplier of Oil to India, China and much of the global south with Indonesia, Thailand, Bangladesh, Pakistan all seeking Russian crude. Despite America’s dominance of European Gas after Nord stream pipeline sabotage, Russian gas continues to flow to Europe and remains critical for Europe’s energy security.

Even close partners show hesitation. Europe and the UK, while heavily dependent on US LNG (with volumes exploding 16-fold since 2019 and long-term contracts in place), are quietly pursuing alternatives for Russian-origin oil, jet fuel, and diesel through third-country intermediaries, shadow fleets, and refined product rerouting. High LNG prices continue to pressure European industry, incentivizing diversification despite diplomatic commitments.

The most significant challenge is America’s inability to resolve the Strait of Hormuz crisis, now stretching into months. This prolonged impasse resembling America’s “Suez moment” has triggered record SPR drawdowns. Global strategic reserves fell by a net 210.7 million barrels from March to end-May 2026, with the US releasing around 50 million barrels. Inventories have dropped to 384.1 million barrels, risking critically low levels by mid-2026 and pushing domestic gasoline prices above $4 per gallon. Gulf producers have suffered massive export losses, while physical market tightness persists despite increased output from the US, Russia, Brazil, and others.

This situation exposes the limits of US leverage in contested maritime chokepoints and accelerates hedging behaviours. While the US has gained short-term market share and strengthened its position as a swing supplier, the strategy risks long-term fragility of depleted buffers, alienated partners, and heightened volatility.

In summary, America’s ambitious restructuring for the AI age confronts the enduring realities of multipolarity. China, India, and Russia’s pursuit of autonomy, Europe’s quiet diversification, and the unresolved Hormuz crisis suggest that a fully US-centric energy order remains contested. Sustainable outcomes will require balancing assertive export diplomacy with multilateral de-escalation and genuine spare capacity investments. The coming months will test whether this realignment delivers stability or entrenches fragmentation in global energy markets.

References

1. Russian pipeline gas to EU: ~165 bcm (2019/2021 peak) to ~20 bcm by 2025 — EU Consilium (updated 2026).

2. US LNG exports to Europe: sharp rise to record levels (~10.3 bcf/d in 2025) — EIA Natural Gas Monthly (Apr 2026).

3. EU-US trade deal: $750 billion in American energy purchases through 2028 — European Commission (Jul 2025) / White House.

4. IEEFA projection: US could supply ~80% (~115 bcm) of EU LNG by 2030 — IEEFA Report (Jan 2026).

5. Growing US share in India’s LNG imports (Kpler data, 2025–May 2026) — Kpler Market Reports (2026).

6. India US LPG imports surge Dec 2025–May 2026 (Kpler volumes) — Argus Media / Kpler (Jan 2026).

7. Hormuz 2026 disruptions: major Gulf export losses, US response — JPMorgan / Kpler / IEA (Apr–May 2026).

8. Global oil inventories: 8.4B barrels start-2026 → 7.6B stress (Jun) → 6.8B floor (Sep) — JPMorgan Commodities Research (May 2026).

9. Global SPR net draw Mar–May 2026 — EIA / IEA Coordinated Reports (Apr 2026).

10.US SPR: ~415 mb early 2026 → ~365–384 mb late May 2026 — EIA Weekly Petroleum Status Report (May 2026)

The trajectory is right. The pace is wrong. What the piece underweights is the freight asymmetry. A Yamal cargo to India runs four times the voyage length of one to Europe, and the landed economics change with it. The realignment is not a clean substitution. It is a series of margin squeezes hiding inside headline flow numbers.